Clarity. Context. Confidence.

.jpeg)

Performance Meets Purpose: The Strategic Advantage of Charitable Donation Accounts

INTRODUCTION:

The challenge of turning purpose into practice…

Unique among financial institutions, credit unions exist to serve members and communities. This mission-driven purpose demonstrates the difference between not-for-profit credit unions and shareholder-serving banks.

Charitable giving is a proof point of the credit union brand.

As those in the industry readily know (especially credit union leaders and board members), surplus earnings are returned to members and communities through lower fees, better rates, and community contributions. And this ultimate contribution to the community makes charitable giving a visible extension of the member-first, mission-driven identity of credit unions.

Every day across America, credit unions give back through direct donations to local nonprofits, schools, food banks, and community organizations. Credit unions sponsor events, scholarships, and financial literacy programs. Staff and leadership contribute volunteer hours. Support is also provided for local development programs, housing, and disaster relief. Finally, credit unions work in partnerships with national causes like Children’s Miracle Network Hospitals.

Designed to support the life-saving work of CMN Hospitals, the movement-wide Credit Union for Kids program is perhaps the most high-profile example of how credit unions deliver on the commitment of giving back.

According to CMN Hospitals, credit unions have collectively raised $225 million for affiliated children’s hospitals since 1996 — and $18.7 million in 2024 alone.

As the third largest fundraising partner for CMN Hospitals, credit unions “fund breakthrough research, numerous programs and services, and construction of new facilities.”

In terms of dedication to the total wellness of the families and communities they serve, credit unions can make a legitimate claim of leadership among all financial service providers. The Credit Unions for Kids initiative offers undeniable proof. Credit unions do make a real difference in the real lives of real people.

So, by shaping how credit unions are perceived, charitable giving enables credit unions to separate themselves from other financial service providers. In a digital-first marketplace where services sometimes look more and more commodified and undifferentiated, the human touch of “people helping people” can make a real difference in the eyes of consumers.

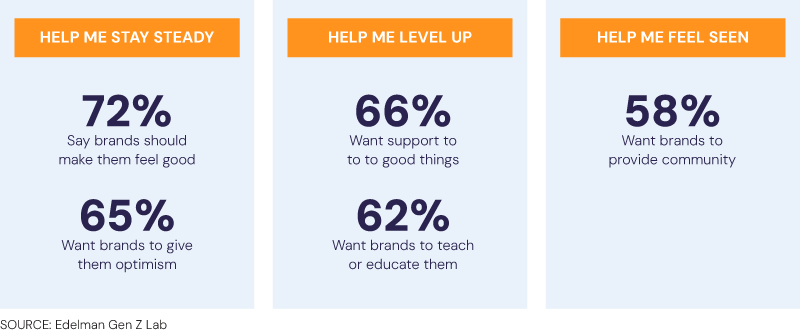

This point is especially important to consider when thinking about reaching the next generation of members. “Given their proximity, brands have a unique opportunity to lean in and show up for Gen Z,” states a recent study from the Edelman Gen Z Lab.

According to Edelman, Gen Z favors brands that “deliver for them, improve their quality of life, and help them make an impact in the world.”

If credit unions aim to bond with the Gen Z members in more empathetic and hyper-personalized ways, a demonstrated dedication to giving could help supply the glue.

However, while it’s always worth celebrating what makes credit unions different, making a difference through charitable giving doesn’t just happen. At the ground level, each credit union must turn its mission-driven purpose into a business practice. This means that the feel-good dedication to “people helping people” promoted in the front of the house has to translate into dollars and cents on the balance sheet in the back office.

Simply put, charitable giving requires a real investment.

But increasingly, finding funds to make this investment in a meaningful manner is no small ask.

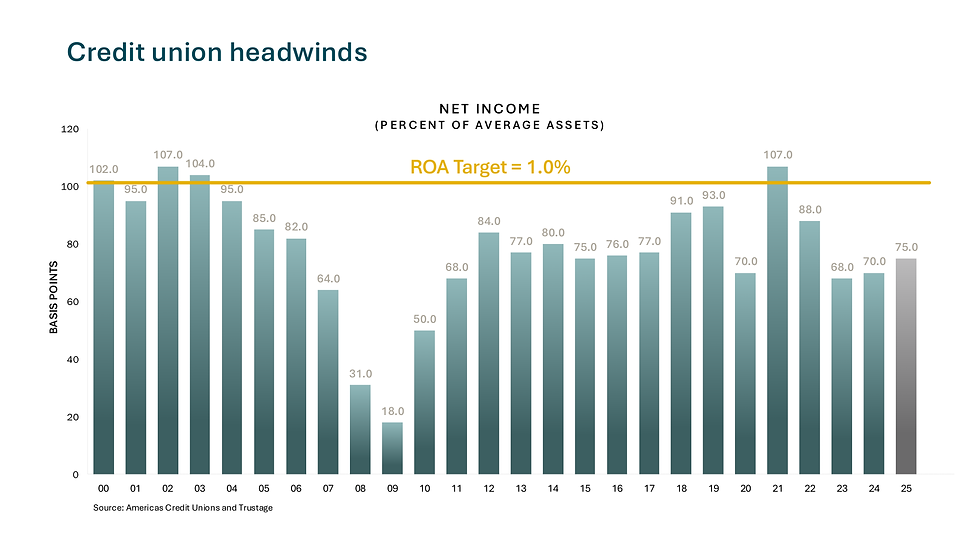

Credit unions have been fighting headwinds for over twenty years.

Margin compression is real, and for many credit unions, underperforming assets and underwater securities are dragging down returns.

Also, despite whatever membership might be gained through affinity with the credit union brand, with earnings and market share trending below target, member growth alone won’t necessarily fix ROA.

The industry target for sustainability is a 1.0% return on assets, but most years since 2000, credit unions have fallen short. Even after a brief spike during the pandemic, we continue to remain below the ROA target.. That gap puts long-term pressure on your ability to reinvest in your mission. But this isn’t just about an industry ratio — it shows up in very real ways for your people, your members, and your community.

Even though the mission remains non-negotiable, as prudent financial stewards of member-owned assets, credit unions must always have a sharp eye on the bottom line.

So, if giving is a given, the question is how might credit unions with tightly wound operations best optimize their investments in charitable giving in the most cost-effective and sustainable ways possible?

The “supercharged” CDA Solution

One answer to this question just might be in the form of an option already — and exclusively — available to all federal credit unions: Charitable Donation Accounts or “CDAs.”

The NCUA lists CDAs among preapproved “incidental powers… necessary or requisite to carry on a credit union’s business.”

In official terms, a CDA is defined as a hybrid charitable giving and investment account authorized under 12 CFR 721.3(b) (2). It permits investments that may otherwise be impermissible, provided the account’s primary purpose is charitable, and any return to the credit union is incidental to that purpose.

In simpler English, CDAs are NCUA-approved investment vehicles that allow credit unions to increase yield on a limited portion of their assets — up to 5% of net worth — as long as at least 51% of earnings are directed to qualified 501(c)(3) charities within five years.

As many credit union leaders know, there’s only so much that can be done from operating funds in regard to charitable donations. But with a CDA, operating funds are untouched. Also, based on the regulatory guidelines governing CDAs, up to 49% of the return on CDA investments can actually be retained to support credit union operations!

Properly structured, CDAs enable credit unions to amplify community giving while maintaining full compliance and safety and soundness standards.

CDAs are not a departure from the cooperative mission. They are an innovation within it — turning underperforming assets into sustainable funding for charitable and community programs.

The outcome math of CDAs. Let’s do the numbers.

Traditionally, charitable giving by credit unions uses after-expense dollars. In contrast to traditional practice, CDAs provide earnings generated from invested assets. In some cases, the CDA model can triple charitable budgets — without affecting operations.

In fact, CDAs can actually create a self-funding engine for charitable giving.

So, in terms of actual dollars, what kind of outcomes could a credit union expect to get from a Charitable Donations Account?

Here’s an example of what a credit union might see with $2 million invested in a CDA:

CDAs provide proof of value, which means that credit unions can show both their boards and their members how every dollar invested in a CDA delivers measurable outcomes.

Gerber Federal Credit Union of Newaygo County, Michigan, is one such credit union that can attest to the measurable advantages and transformational effect of CDAs.

With guidance from Acumen Financial Advantage and several months of internal study, Gerber FCU opened its CDA in November 2024. Since implementing their CDA strategy, the credit union has been pleased by the “significant impact on both [their] charitable giving and overall financial strategy,” according to John Buckley, Gerber FCU’s President & CEO.

Because of their CDA, Buckley says that they now “project to triple” charitable giving per year.

Most importantly, Gerber FCU’s decision to implement their CDA strategy will benefit the kids and families of Newaygo County for years to come.

“It allowed us to make a commitment to our local community museum to support all their children’s programming for five years,” says Buckley. “And that is not something we could have done under our prior investment and marketing strategy.”

Before working with Acumen Financial Advantage, we were donating approximately $17,000 annually to nonprofit partners. After implementing their program, we project to triple our charitable giving to $51,000 per year. In addition, we’ve enjoyed an extra $49,000 returned to our bottom line annually — a valuable boost for our financial strength.”

John P. Buckley, Jr. – President & CEO, Gerber Federal Credit Union]

“It allowed us to make a commitment to our local community museum to support all their children’s programming for five years,” says Buckley. “And that is not something we could have done under our prior investment and marketing strategy.”

As the experience of Gerber FCU demonstrates, CDAs let credit unions turn today’s dollars into tomorrow’s impact — multiplying charitable giving without draining annual budgets.

The team from Acumen emphasizes that with the potential to multiply the budget for giving, CDAs can drive both increased community impact and allow for reinvestment in the organization. “In fact, with the right guidance and partner, your organization can conservatively expect to increase your Return on Investment from 4% to 10%.

Notes on CDA Compliance Guardrails

Despite all of the benefits of CDAs, regulatory phrases like “may otherwise be impermissible” might raise a few red flags — or at least a few eyebrows — among credit union board members as they assess the merits of CDA implementation.

To potential skeptics, it should be further emphasized that, in the eyes of NCUA examiners, CDAs are seen as “preapproved as incidental to carry on your business.” This means that CDAs are not a loophole within NCUA regulations.

However, CDAs should not be considered a plug-and-play, set-it-and-forget kind of solution.

Transparency, a documented Board policy, and strict adherence to the “51% rule” are among the keys to proper compliance. Meanwhile, to credit union members, a CDA should demonstrate responsible financial stewardship and their credit union’s honest commitment to maximizing community impact.

Therefore, staying compliant does require attention.

So, how are risk and compliance managed? And what are the regulatory limits?

When it comes to risk, compliance, and key regulations, here are several important points worth noting about CDAs:

-

Accounts are fully auditable and transparent. Fair value is calculated quarterly and verified by third-party custodians.

-

The credit union maintains control via Board-approved policies governing investment selection, liquidity, and risk tolerance.

-

CDA assets carry a 100% risk weight for capital purposes, which is standard and expected.

-

Total CDA investments can’t exceed 5% of net worth at any time.

-

At least 51% of cumulative earnings must be donated to 501(c)(3) organizations every 5 years.

-

The CDA must be a segregated custodial account (or trust) specifically identified as a Charitable Donations Account.

-

The Board must adopt written CDA policies, review them annually, document risk tolerances, and charity guidelines.

Of course, each participating credit union selects its own 501(c)(3) beneficiaries, and the credit union’s board retains full discretion over charitable recipients and timing.

It takes best practices

Currently serving more than 200 credit unions and experienced in the successful implementation and administration of CDAs, Acumen Financial Advantage builds the business case for CDAs by taking “an empathetic, educational approach to make sure that the concept fully makes sense,” according to Mark Axmacher, Vice President & CIO at Acumen.

It’s worth taking a brief look at some of the more noteworthy best practices related to risk management and oversight that Acumen recommends for credit unions considering CDA implementation.

These recommended best practices include:

-

Understanding the 5% net worth limitation: This 5% cap is crucial, as it limits the total amount that a credit union can invest in higher-risk assets under the CDA structure.

-

Regular compliance monitoring: Credit unions should maintain detailed records that document their net worth calculations, CDA investment decisions, and compliance with the 5% cap, as well as verify that at least 51% of the income generated is properly donated to charities that meet NCUA qualifications.

-

Developing a comprehensive Investment Policy Statement (IPS): A detailed IPS should outline the types of investments, risk tolerance levels, and expected returns. This document serves as a guide for portfolio management and ensures that all investment activities align with regulatory requirements and the credit union’s strategic goals.

-

Transparent reporting: Credit unions should provide regular reports to their boards and regulators, detailing the current net worth, CDA investments, and the percentage of net worth allocated to CDAs. This transparency helps prevent inadvertent non-compliance.

Furthermore, there are a couple of misconceptions about CDAs to be aware of…

First, investments don’t have to be high-risk to be meaningful. And second (and perhaps more significantly), the 5% of net worth that goes into the CDA can’t be used to offset employee benefit expenses. As Acumen’s Mark Axmacher puts it, the 5% of net worth allowed for the CDA is a “standalone bucket of money.”

The industry’s best kept secret?

Implementation of a charitable donation account CDA is a fairly direct process for credit unions. Approval requires a vote by the credit union’s leadership and board, which also sign off on the specific investment strategies that would be used to fund the CDA.

And yet…

Even though the benefits to credit unions and their communities are easy to see, and it’s relatively simple to set up charitable donation accounts, perhaps the most curious aspect of the CDA story to date is how few credit unions actually have them.

The NCUA established the rules permitting credit unions to fund CDAs in 2013. Ten years later, a 2023 analysis by the NCUA stated that there were “only 136 federal credit unions utilizing CDAs.” (15) Today, Scott Hinkle of Acumen estimates only about 5% of credit unions use them.

Acumen is committed to spreading the word about the singular opportunity that CDAs offer to credit unions. Their “Credit Union Impact Report” provides a customized analysis of how a credit union might strengthen financial performance “to reduce employee costs, improve ROA, and grow charitable giving.”

Acumen views community impact as a pillar of the credit union mission — and a CDA investment is central to any strategy designed to maximize the impact of credit union assets utilized on behalf of members and their communities.

CONCLUSION:

The win-win-win of CDAs

From the industry-wide support of organizations like Children’s Miracle Network Hospitals to local support of a children’s museum in Newaygo County, Michigan, credit unions demonstrate the “people helping people” philosophy every day, all day.

So, for credit unions that are truly dedicated to their mission, but searching for a way to deliver on the promise, it might be heartening to know that there is an innovative tool that can not only help them deliver, but can also turn their commitment to purpose into a sound business practice.

An option for credit unions since 2013, and recently amended by the NCUA to allow charitable donations to veterans’ organizations, a CDA can reinvigorate a credit union’s identity within its community — and also benefit the balance sheet.

As the team at Acumen Financial Advantage can show, CDAs can have a measurable and almost immediate impact on a credit union’s performance. In some cases, a strategically implemented CDA can triple a credit union’s giving potential.

In the end, credit unions, their boards, and members can all win with CDAs.

For credit unions, CDAs create operational efficiency, providing the foundation for a sustainable charitable giving program designed to grow over time.

For executives and boards, CDAs offer plain-language ROI, regulatory clarity, and scalable giving strategies.

For member relationships and communities, they deliver proof that credit unions are more than financial institutions — they are catalysts for positive change.

Every credit union has a great story and a great story to tell,” says Scott Hinkle. “A charitable donation account gives them the opportunity to go on the offense, to really get out there into the community, [and] get their story heard by people who have never heard the story before. And ultimately… that’s going to drive member growth, bring more assets to the institution, and you’ll be a better servant to your community.”

See the numbers on how a CDA can transform your credit union’s giving capacity. Apply for your complimentary custom impact report at Acumenfa.com/plans/cda

Building on our growth strategy offering, our services include:

Sales

CX Diagnostics, Audience Analysis & Journey Mapping

Sales & Lead Generation

Sales Tool Analysis & Unified Process Enablement

Sales Performance & Optimization

Marketing

Omni-channel Marketing Strategy & Execution

Content Planning & Delivery

Experiential and Event Planning & Production

Thought Leadership Content & Speakerships

Business

Business Case Development & Modeling

Finance Strategy Modeling

Brand Development, Design & Strategy

Product Performance & Optimization